By admin

January 23, 2026

By admin

January 23, 2026

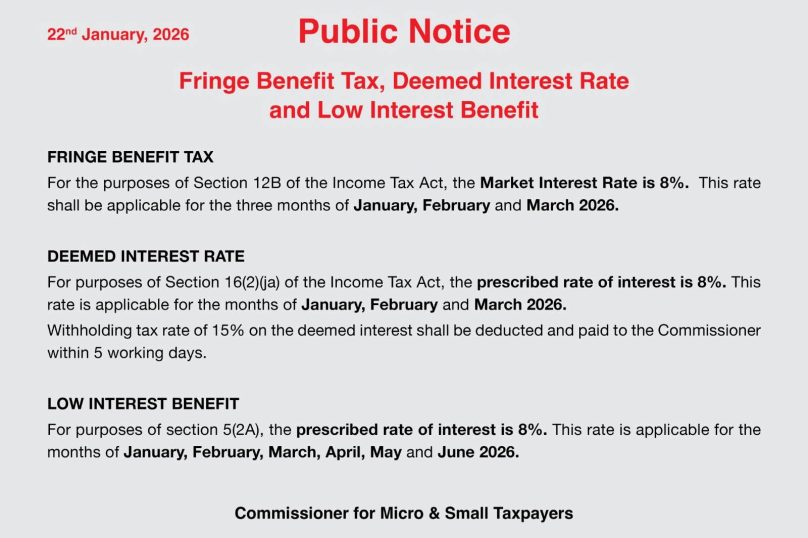

The Kenya Revenue Authority (KRA) issued a public notice dated 22nd January 2026 outlining the applicable market and prescribed interest rates for purposes of Fringe Benefit Tax (FBT), Deemed Interest, and Low Interest Benefit under the Income Tax Act.

This notice is particularly important for employers, company directors, shareholders, SMEs, payroll managers, and finance professionals, especially where loans or advances are issued at low or zero interest.

In this article, Juma Auditors explains what the notice means, who is affected, and how businesses can remain compliant.

Fringe Benefit Tax (FBT) – What Employers Need to Know

What Is Fringe Benefit Tax?

Fringe Benefit Tax applies to non-cash benefits provided by an employer to employees. One common benefit is interest-free or low-interest loans.

KRA Market Interest Rate for FBT (2026)

Under Section 12B of the Income Tax Act, KRA has set:

- Market Interest Rate: 8%

- Applicable Period: January, February and March 2026

Tax Implication

If an employee loan attracts interest below 8%, the difference is treated as a taxable fringe benefit.

The employer must:

- Calculate the fringe benefit

- Pay Fringe Benefit Tax monthly

- Remit the tax to KRA by the 10th of the following month

Deemed Interest Rate – Loans to Directors & Shareholders

What Is Deemed Interest?

Deemed interest applies when a company advances interest-free or subsidized loans to:

- Directors

- Shareholders

- Related parties

KRA assumes the company should have earned interest income.

KRA Prescribed Rate for Deemed Interest (2026)

Under Section 16(2)(ja) of the Income Tax Act:

- Prescribed Interest Rate: 8%

- Applicable Period: January, February and March 2026

- Withholding Tax Rate: 15%

- Payment Deadline: Within 5 working days

Practical Impact

Companies must:

- Compute the deemed interest

- Deduct 15% withholding tax

- Remit the tax promptly to avoid penalties and interest

Low Interest Benefit – Extended Period in 2026

What Is Low Interest Benefit?

Low interest benefit arises where loans are advanced at rates below the prescribed interest rate, creating a taxable benefit.

KRA Prescribed Rate for Low Interest Benefit (2026)

Under Section 5(2A) of the Income Tax Act:

- Interest Rate: 8%

- Applicable Period:

January, February, March, April, May and June 2026

This affects employers and companies offering subsidized loan facilities.

Why the KRA Notice Is Important for Businesses

This public notice:

- Sets a clear benchmark interest rate

- Eliminates ambiguity in tax computations

- Helps businesses align loan policies

- Reduces audit and compliance risks

Failure to comply may result in:

- Additional tax assessments

- Penalties and late payment interest

- Increased scrutiny during KRA audits

Key Compliance Steps Businesses Should Take

Businesses should immediately:

- Review all employee, director, and shareholder loans

- Compare loan interest rates against the 8% benchmark

- Recalculate Fringe Benefit Tax where applicable

- Deduct and remit withholding tax on deemed interest

- Update payroll and accounting systems

- Maintain proper loan documentation

How Juma Auditors Supports Your Compliance

Juma Auditors assists businesses by:

- Reviewing loan structures and tax exposure

- Computing Fringe Benefit Tax accurately

- Assessing deemed interest and withholding tax obligations

- Advising on tax-efficient loan arrangements

- Supporting KRA audits and compliance reviews

Conclusion

The KRA public notice issued on 22nd January 2026 reinforces the importance of correct tax treatment of loans and benefits. With the prescribed interest rate set at 8%, businesses must proactively review their arrangements to remain compliant and avoid penalties.

Need Expert Tax Advice?

📞 Phone: +254 725 948 551

📧 Email: info@jumaauditors.co.ke

🌐 Website: www.jumaauditors.co.ke

Juma Auditors – Trusted Tax & Compliance Advisors