By admin

April 15, 2026

By admin

April 15, 2026

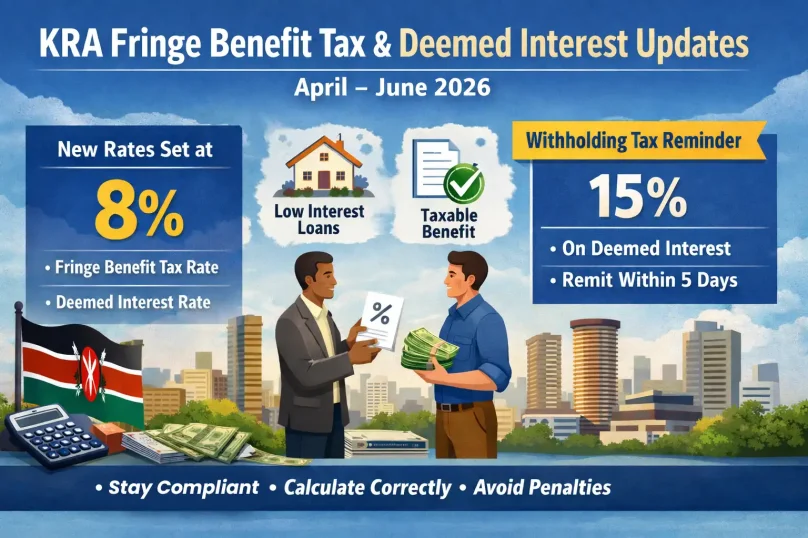

If your business offers staff loans or any interest-based financial benefits to employees, the Kenya Revenue Authority (KRA) has an update that directly affects your tax obligations.

For the period April to June 2026, KRA has set both the Fringe Benefit Tax (FBT) market rate and the deemed interest rate at 8%. Here’s what that means in plain terms — and what you need to action.

What is Fringe Benefit Tax (FBT)?

FBT applies when you give an employee a benefit that isn’t part of their salary. The most common example is a staff loan offered at a lower interest rate than the KRA market rate.

The logic is simple: if your employee is getting a cheaper loan than they would from a bank, KRA treats that “discount” as a taxable benefit.

How it works: If your company charges an employee 3% interest on a loan, but KRA’s prescribed rate is 8%, the 5% gap is treated as a taxable benefit — and FBT applies on that difference.

What is Deemed Interest?

Deemed interest kicks in when a loan is issued with zero interest or at a rate below the KRA threshold. Rather than ignoring the missing interest, KRA “deems” that interest should have been charged — and taxes it accordingly.

This closes a common loophole where businesses might otherwise use interest-free loans to move money without triggering tax.

Current rate: 8% (April–June 2026)

The Withholding Tax Obligation You Can’t Miss

Once deemed interest is calculated, there’s an additional step many businesses overlook:

- Withholding tax rate: 15% on the deemed interest amount

- Deadline: Within 5 working days

This isn’t optional. Failure to deduct and remit on time can result in penalties and interest charges from KRA.

A Practical Example

Let’s say an employee receives a loan of KES 1,000,000, and your company charges them 2% interest.

| Item | Detail |

|---|---|

| KRA prescribed rate | 8% |

| Rate charged | 2% |

| Taxable difference | 6% |

| Taxable benefit amount | KES 60,000 |

| Withholding tax (15%) | KES 9,000 |

That KES 9,000 must be remitted to KRA within 5 working days of the relevant period.

Does This Affect Your Business?

These updates are most relevant if your business:

- Offers loans to employees (at any interest rate)

- Provides financial benefits tied to interest rates

- Has related-party lending arrangements — for example, loans between a parent company and a subsidiary

If none of these apply, the direct impact on your business is minimal.

What You Should Do Now

To stay on the right side of KRA:

- Review any outstanding staff loans — check the interest rate being charged against the 8% threshold

- Calculate FBT and deemed interest for the April–June 2026 period

- Deduct and remit 15% withholding tax within 5 working days where applicable

- Update your payroll or accounting system to reflect the new rate

- Keep records — documentation is your best protection in the event of an audit

Why Does KRA Change These Rates?

These rates are reviewed quarterly to stay in step with market lending conditions, economic trends, and monetary policy. The goal is to ensure tax calculations reflect the real cost of borrowing — so businesses can’t engineer artificially cheap loans to sidestep tax obligations.

Bottom Line

The 8% rate for both FBT and deemed interest is straightforward — but the compliance steps attached to it require attention. Miss the withholding tax deadline, and the penalties can quickly outweigh the administrative effort it would have taken to stay compliant.

If you’re unsure how these rules apply to your specific loan arrangements, it’s worth getting a quick review from a tax advisor before the quarter closes.

Have questions about your business’s tax position? Speak to a qualified tax professional who can walk you through the numbers specific to your situation.