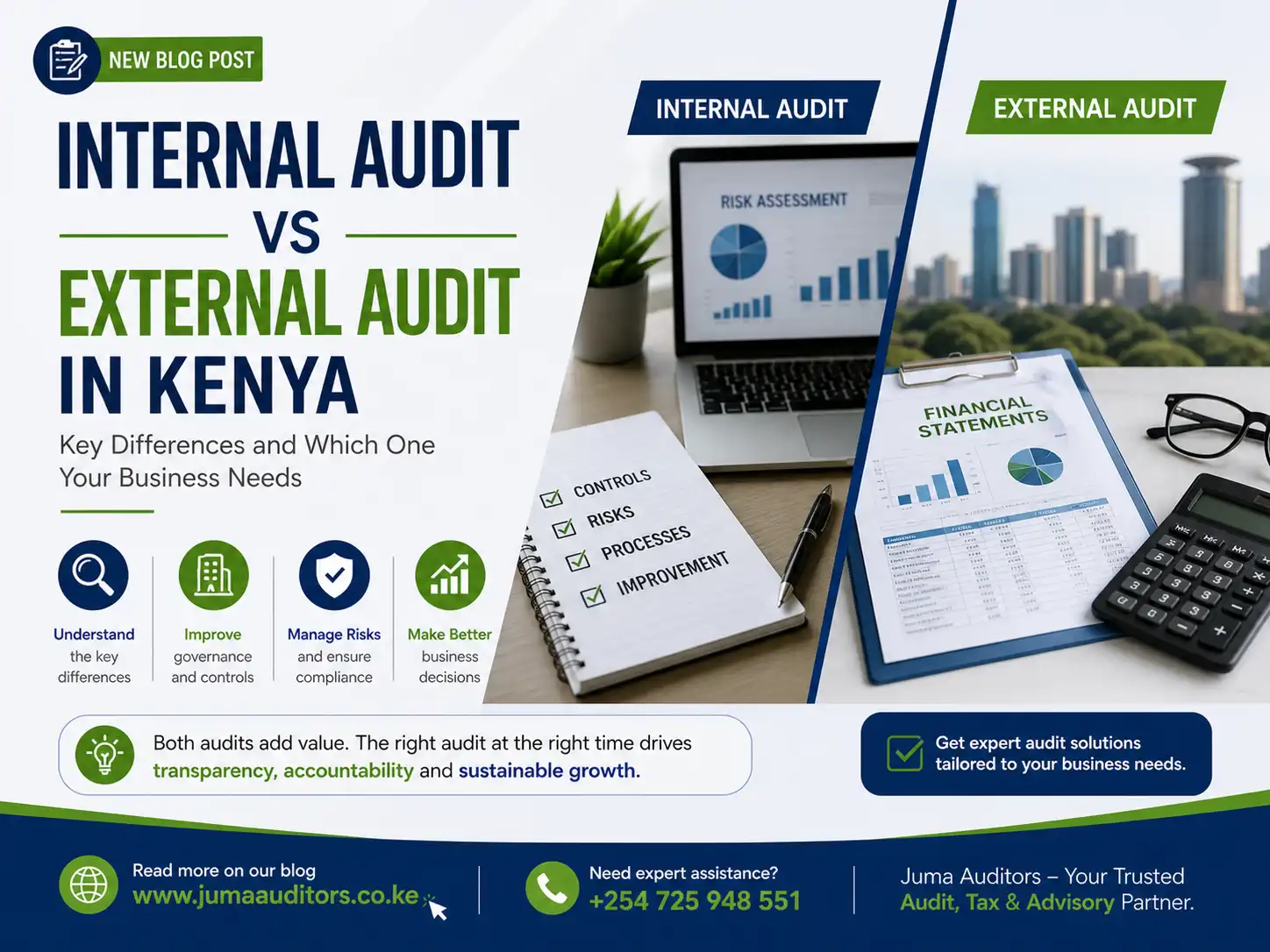

By admin

February 6, 2026

By admin

February 6, 2026

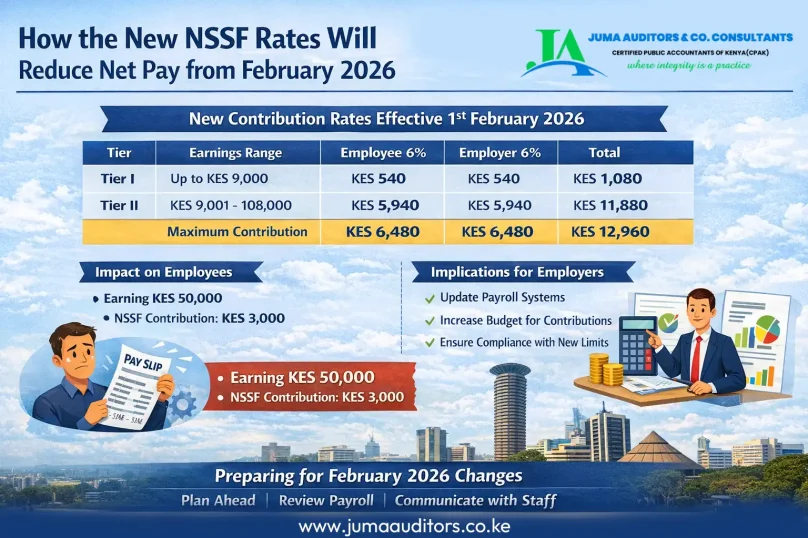

The NSSF Act, 2013 introduced a two-tier contribution system designed to enhance retirement savings for Kenyan employees. Since its rollout began in February 2023, the framework has been implemented in phases. The February 2026 revision marks the fourth phase, with future adjustments to be effected through Gazette Notices.

Effective 1st February 2026, the National Social Security Fund (NSSF) contribution structure will change materially. While the statutory contribution rates remain unchanged at 6% for employees and 6% for employers, the Lower Earnings Limit (LEL) and Upper Earnings Limit (UEL) will increase significantly. This adjustment will lead to higher monthly deductions for employees and increased statutory costs for employers.

Key Changes Effective February 2026

| Tier | Earnings Range | Employee (6%) | Employer (6%) | Total |

|---|---|---|---|---|

| Tier I | Up to KES 9,000 | KES 540 | KES 540 | KES 1,080 |

| Tier II | KES 9,001 – 108,000 | KES 5,940 | KES 5,940 | KES 11,880 |

| Total | Maximum Monthly Contribution | KES 6,480 | KES 6,480 | KES 12,960 |

- The Lower Earnings Limit (Tier I) increases to KES 9,000, attracting a monthly contribution of KES 540 each from the employee and employer.

- The Upper Earnings Limit (Tier II) rises to KES 108,000. Earnings within this band will be subject to a 6% contribution from both parties, translating to KES 5,940 each.

- Employees earning KES 108,000 and above will therefore attract a maximum combined NSSF contribution of KES 12,960 per month.

Impact on Employees

The effect on employees will vary based on income levels:

- Lower-income earners will experience minimal changes.

- Middle- and higher-income earners will see increased deductions as the Tier II ceiling expands.

- Although net pay will reduce, employees benefit from enhanced long-term retirement savings.

Illustration

Employee earning KES 50,000

- Tier I: 6% × 9,000 = KES 540

- Tier II: (50,000 − 9,000) × 6% = KES 2,460

- Total Employee Contribution: KES 3,000

Employee earning above KES 108,000

- Tier I: 6% × 9,000 = KES 540

- Tier II (capped): (108,000 − 9,000) × 6% = KES 5,940

- Total Employee Contribution: KES 6,480

Implications for Employers

Employers should take proactive measures to ensure compliance, including:

- Updating payroll systems to reflect the revised earnings limits

- Budgeting for higher statutory contributions

- Ensuring accurate and timely monthly remittances

Employers may also contract out Tier II contributions to a Retirement Benefits Authority (RBA)–registered pension scheme, subject to regulatory approval and compliance.

Conclusion

The revised NSSF contribution structure effective 1st February 2026 significantly broadens pensionable earnings while maintaining the existing contribution rate. Both employers and employees should prepare in advance to facilitate a smooth transition and ensure compliance.

Juma Auditors advises businesses to review payroll configurations, communicate changes early to staff, assess the financial impact on remuneration structures, and seek professional guidance where necessary.